Washington Tax Changes in 2026: Millionaires Tax & Estate Tax Guide

Washington State tax legislation has been a moving target in recent years, with ongoing developments surrounding the capital gains tax, the “Millionaires Tax”, and more recent updates to the estate tax. These Washington tax changes, many of which are still evolving in 2026, have prompted a range of responses. While the financial implications are real, personal values often play an equally important role as some consider relocating to mitigate potential impacts while others remain rooted for family and personal priorities. In this shifting landscape, proper tax planning is becoming even more critical as well as having a foundational planning strategy to maintain tax diversification, allowing individuals and families to stay flexible and adapt as state and federal tax laws continue to change. Below, you will find a high-level overview of what some of these new tax laws are, as well as some strategies that you can employ to mitigate their impact.

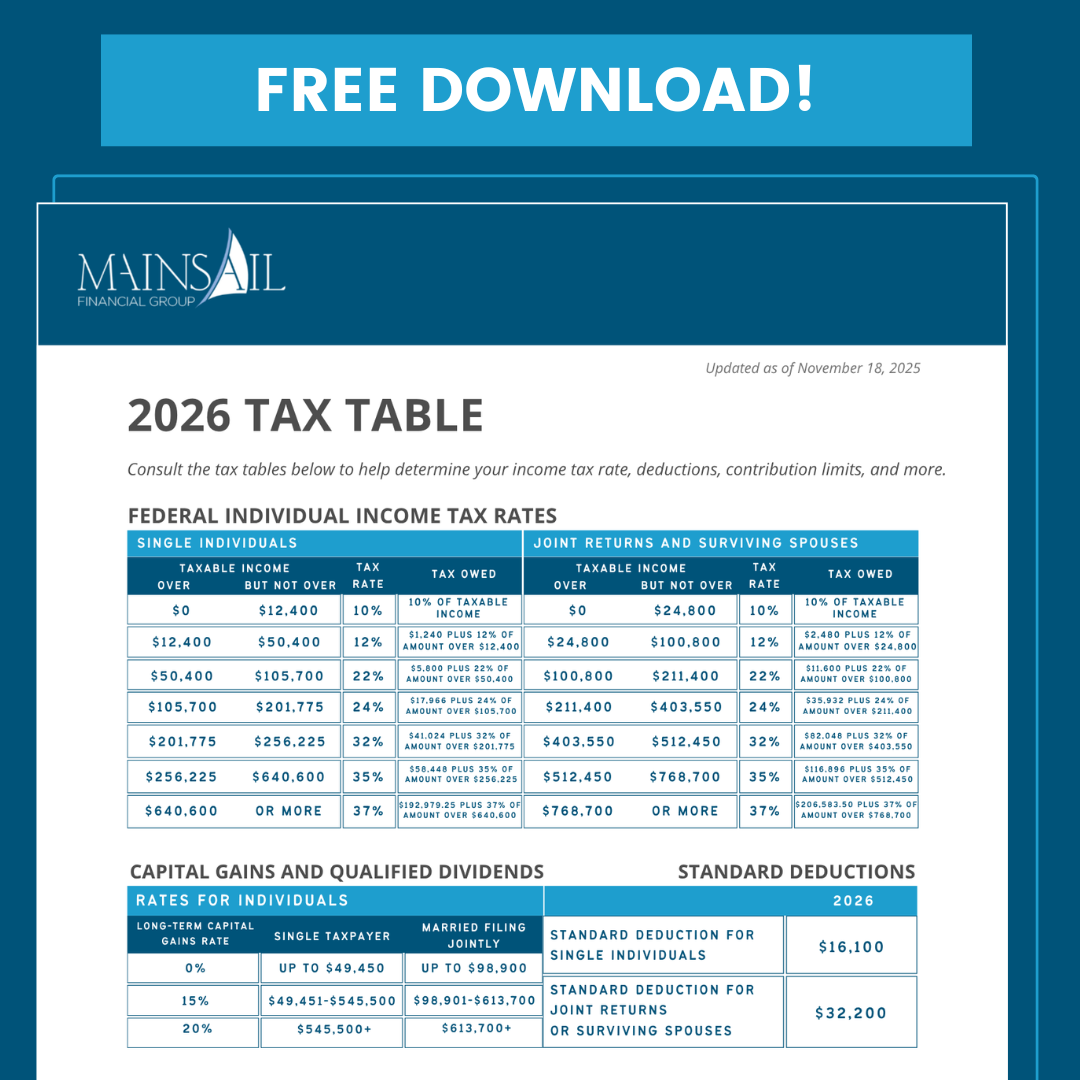

Plan ahead for 2026! Download your complimentary 2025-2026 Tax Table below

Washington State Capital Gains Tax: What’s Changing in 2026

Washington State’s capital gains tax, which has been in effect since 2024, applies a baseline 7% tax on certain realized gains, with a key annual deduction that significantly impacts who is subject to the tax. Currently, individuals can deduct up to $278,000 in capital gains each year (indexed to inflation), meaning the tax generally only applies to gains above that threshold. One interesting thing to note is that deduction is the same whether you are filing single or married filing jointly.

More recently, the structure has shifted from a flat tax to a tiered system, which is 7% on gains up to $1 million and 9.9% on amounts above that level. Notably, the brackets, like the deduction, remain the same regardless of filing status, which differs from many traditional tax frameworks. It is also important to understand that, for now, several common assets are excluded, such as real estate transactions, retirement accounts, and certain small business interests. Given the nuances and evolving nature of the law, it’s important to have a thoughtful long-term approach to managing these taxes.

Washington Millionaires Tax: Who It Affects and How It Works

Washington State’s newly enacted “Millionaires Tax” represents one of the most significant recent developments in the state’s tax landscape. At its core, the policy introduces a 9.9% tax on income. Like the capital gains tax there is a standard deduction that is set at $1 million, with that threshold applying equally to both single filers and married couples filing jointly. Compared to traditional tax structures, this is a bit of an uncommon approach. Taxpayers effectively receive a $1 million deduction, and only income exceeding that amount may be subject to the tax. While there are already lawsuits pending, as of now it is set to take effect in the 2028 tax year, with payments due in 2029.

The scope of this tax is broad, applying to a wide definition of income that includes earned income, capital gains, and pass-through income from businesses or trusts. It primarily targets Washington residents, but non-residents may also be impacted if a portion of their income is derived from or connected to Washington State. This introduces added complexity, particularly for those considering relocation, as simply moving out of state may not fully eliminate exposure to the tax, depending on income sources.

Importantly, the legislation does attempt to mitigate double taxation by coordinating with the state’s existing capital gains tax. However, there are nuanced scenarios where overlap may still occur, especially depending on how different types of income are categorized and reported. Certain exclusions, such as the sale of a primary residence or qualifying business, do apply, but there is still a lot to explore in regard to the details.

Overall, the introduction of this tax underscores a growing need for thoughtful, proactive planning. With a broader definition of taxable income and increasing interaction between different parts of the tax code, individuals, particularly high earners or business owners, will need to be more strategic in how they manage income, structure assets, and plan for future tax exposure.

Are you prepared for taxes in retirement?

For more long-term tax planning strategies, claim your FREE copy of Brandon’s book, Retire by Design!

Washington State Estate Tax Changes in 2026: Exemptions and What to Know

Washington State’s estate tax has seen several recent changes, making it an important aspect to monitor within overall financial planning. Estate planning is critical, no matter the level of complexity.

From a tax perspective, it is helpful to distinguish between the federal and state estate tax systems. Federally, the estate tax exemption is currently around $15 million per person (or $30 million for married couples), with a top tax rate of 40%, and includes a unified structure that accounts for both lifetime gifts and estate transfers.

At the state level, Washington’s estate tax has undergone more noticeable shifts. The exemption was recently increased from just over $2 million to $3 million, with prior changes also introducing steeper, tiered tax brackets. However, based on the latest updates, the state appears to be reverting to the lower tiering structure. Washington state is maintaining the $3 million exemption but removing its inflation adjustment and returning to a top estate tax rate of 20%. These adjustments come after concerns that earlier changes made Washington one of the highest-taxed states for estates, prompting both public feedback and potential behavioral shifts, including relocation considerations.

Even with this reversion, Washington’s estate tax remains a meaningful consideration, particularly when combined with federal rules and reinforces the need for proactive and well-coordinated estate planning.

Estate Planning Strategies for Washington Retirees

As Washington State’s estate tax rules continue to evolve, there are several key strategies individuals can consider helping manage potential exposure. One of the most straightforward is lifetime gifting. Individuals can make annual gifts within federal limits without impacting their lifetime exemption, but even larger gifts can be particularly effective in Washington, since the state does not offer its own lifetime gifting exemption at this time. This creates a meaningful planning opportunity, especially for those whose estates may fall between federal and state thresholds.

Trust planning is another commonly used approach. By transferring assets into an irrevocable trust, individuals may be able to remove those assets, and any future growth, from their taxable estate. However, this requires giving up control, and large transfers are still considered gifts for tax purposes. Revocable trusts, on the other hand, offer flexibility and control but do not provide estate tax benefits, making it important to understand which structures align with your goals.

A critical nuance in Washington State is the lack of “portability” between spouses. Unlike the federal system, where a surviving spouse can utilize a deceased spouse’s unused exemption, Washington does not allow this. As a result, if proper planning isn’t in place, families risk losing part of their combined exemption, potentially leading to avoidable estate taxes. This makes coordinated estate planning, often involving trusts or other legal structures, an essential and relatively straightforward step to ensure both spouses’ exemptions are fully utilized.

What these 2026 Tax Changes Mean for Washington Retirees

Washington State’s tax landscape continues to evolve, with key developments across many areas of the tax landscape including capital gains tax, the newly introduced Millionaires Tax, and recent updates to the estate tax. While these changes represent a meaningful shift, it is important to recognize that some aspects, particularly the Millionaires Tax, may face ongoing legal challenges that could impact how (or if) they are ultimately implemented. Regardless of the outcome, the broader trend is clear: the state’s tax code is becoming more complex, and long-term planning is more important than ever. Taking a proactive, strategic approach can help ensure you remain flexible and well-positioned as new developments unfold.

Advisory services offered through Mainsail Financial Group, LLC, a Registered Investment Adviser. For informational purposes only, not intended as tax advice. Please consult a tax professional when appropriate.